Manufacturing Update - 26 November 2024

Insights from articles and reports of interest on manufacturing technology, management, policy, and economics in the US and abroad

Table of contents for article summaries below:

Why higher R&D spending is not translating into more rapid productivity growth in the US

Donald Trump’s shake-up of EV rules would be ‘huge positive’ for Tesla

Trump Tariff Policies, Two Perspectives:

a. Donald Trump’s trade remedies reflect America’s troubled realities

b. Trump Tariffs

Some Fear Factory Boom Could Suffer Under Trump

Why Venture capital is Indispensable for US Industrial Strategy – Activating Investors to Realize Disruptive National Capabilities

1. “Why higher R&D spending is not translating into more rapid productivity growth in the US,” Ufuk Akcigit, IMF, Finance and Development Magazine, Sept. 2024 (excerpted in Tooze, Chartbook, 11/21/24)

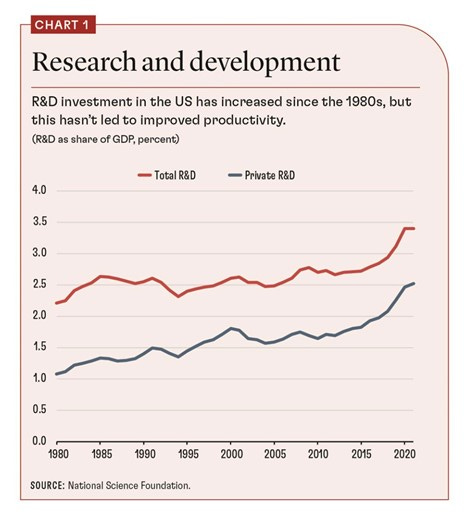

In the 1980s, total US R&D investment represented 2.2 percent of GDP. Today, that figure is 3.4 percent, according to the National Science Foundation (see Chart 1). Private R&D spending by businesses more than doubled, to 2.5 percent of GDP from 1.1 percent.

Based on conventional economic models, that kind of increase in R&D spending should have led to accelerated economic growth rather than the slowdown that actually occurred. Productivity growth between 1960 and 1985 averaged 1.3 percent. Over the subsequent three and a half decades, gains in productivity fell below that average, except for a brief uptick in the early 2000s, and annual growth has generally been declining.

Over the past two decades, there has been a notable reallocation of innovative resources toward large, established companies, Goldschlag and Akcigiti documented in 2022. At the beginning of this century, roughly 48 percent of American inventors worked for these big incumbent companies—those that are more than 20 years old and employ more than 1,000 workers. By 2015, that figure had surged to 58 percent, marking a significant shift in where the nation’s innovative talent is concentrated.

The evidence suggests that while the US is investing more in R&D, the concentration of resources among large businesses has led to diminishing returns in terms of productivity growth. If figure 1 showed something like rates of obesity, air pollution, or violent crime, then we’d be celebrating the decline we’ve experienced since 2011. But it is a graph of the change in labor productivity in U.S. manufacturing, which grew steadily throughout the post-war era until 2010, and since then has slid. Let me say this again: U.S. manufacturing is becoming less productive.

Excerpted with edits; more at: https://www.imf.org/en/Publications/fandd/issues/2024/09/the-innovation-paradox-ufuk-akcigit

2. “Donald Trump’s shake-up of EV rules would be ‘huge positive’ for Tesla,” Claire Bushey, Financial Times, Nov. 14, 2024

Donald Trump’s criticism of electric vehicles looks likely to lead to the end of government subsidies for consumers who buy them, boosting Elon Musk’s Tesla by hitting its rivals with greater losses. The president-elect has said EVs would spell “complete obliteration” for the US car industry, even as adoption for the vehicles has climbed in other parts of the world, particularly China.

Trump said in July when he accepted the Republican nomination that he would “end the electric vehicle ‘mandate’ on day one”, referencing proposed emissions rules that President Joe Biden’s administration had eased four months earlier. While Tesla is making money from its EVs, rivals’ losses on them have been narrowed by consumer tax credits worth up to $7,500 under Biden’s Inflation Reduction Act. “A Trump presidency would be an overall negative for the EV industry,” said Wedbush analyst Dan Ives. “However, for Tesla, we see this as a huge positive.”

Tesla has added more than $300bn in market capitalization since election night, a figure larger than the value of many rivals. “Take away the subsidies,” Musk posted in July on X, the social media site that he owns. “It will only help Tesla.” Trump’s election could also lead to swifter regulatory approval for autonomous driving technology, helping Tesla and other groups developing self-driving cars.

Excerpted with edits; more at: https://www.ft.com/content/a8799b8e-d84d-4a1b-bcea-31920ca7c94f

3. Trump Tariff Policies, Two Perspectives:

3a. “Donald Trump’s trade remedies reflect America’s troubled realities,” Robert Lighthizer, Opinion, Financial Times, Nov. 1, 2024 (The author was US Trade representative in the prior Trump Administration and a strong tariff advocate)

Critics of Donald Trump’s popular tariff proposals claim they will be inflationary and harm the economy. The fact that this never happened during Trump’s first term, when we raised tariffs, is reason enough to be skeptical of such criticisms. But the problems with them go deeper. Few of those who criticize these tariffs stop to consider what the brand of free trade they have promoted has done to America and to American workers over the past 30 years.

In the past three decades we have lost millions of jobs, many of them high- paying manufacturing ones. We have seen median wages stagnate, except for a period during Trump’s administration. Communities across America have been destroyed. The two-thirds of our workforce with only high school diplomas live on average over eight years less than college graduates.

We have also seen a growth in income and wealth inequality that is alien to America. The top 1 per cent of our citizens now have more wealth than the middle 60 per cent — another first. In the past 60 years, families in the top 1 per cent have seen their wealth grow from 36 times that of families at the 50th percentile to 71 times their wealth.

At the macroeconomic level the results have been equally alarming. We have run up giant trade deficits every year for decades. This transfers trillions of dollars of our wealth overseas in return for current consumption. Staggeringly, foreigners now own over $22tn more of American assets than Americans own throughout the world.

We are also losing the future innovation that goes with manufacturing. We’ve essentially lost the nuclear, electronics, textiles, and chemicals industries. I could go on and on. Innovation has lagged too. The Australian Strategic Policy Institute found that the US is behind China in 57 of 64 critical technologies.

Economic growth has also slowed. In the two decades before 1980 our economy grew faster than 3 per cent in 14 separate years. In the period between 1980 and 2000 it exceeded 3 per cent another 14 times. Since 2000 that has only happened three times and one was the abnormal Covid recovery year.

The trading system is not the only culprit in this tragedy, but it is a major one. Economists’ free trade prescriptions fail because they do not reflect modern reality. Classical economists told us that a country exports in order to import. That is how it gets the “trade benefit” — Portuguese wine for English woollens per Adam Smith. We got the theory of comparative advantage from David Ricardo — a country produces what market forces say it makes best, not everything. Yet, what we have seen in recent decades is countries adopting industrial policies that are designed not to raise their standard of living but to increase exports — in order both to accumulate assets abroad and to establish their advantage in leading edge industries. These are not the market forces of Smith and Ricardo. These are the beggar-thy-neighbor policies that were condemned early in the last century.

Countries that run consistently large surpluses are the protectionists in the global economy. Others, like the US, that run perennial huge trade deficits are the victims. They end up trading their assets and the future income from those assets for current consumption. Many economists will say this is all the fault of the victim, and that the US has too low a savings rate. Of course, the trade deficit is equal to the difference between a country’s investment and its savings, but the causation runs the other way. Foreign industrial policy creates the deficits and with investment being set by demand for domestic investment, savings must go down. The problem is not the concomitant savings rate. It is the predatory industrial policies.

Facing a system that is seriously failing our country, Trump has decided that action must be taken. There are essentially three ways to bring about fairness and balance, and so help businesses and workers. First, the US could impose a system of import/export certificates. Second, it could legislate a capital access fee on inbound investment, meaning that buying up our assets would be more expensive. Or, finally, the US could use tariffs to offset the unfair industrial policies of the predators.

We know from the first Trump administration that the last of these remedies works. Manufacturing was up, imports were trending down pre-Covid and workers had the highest real wage increase on record. It is time for a change. Our trading partners, particularly those with large trade surpluses, shouldn’t blame us for shifting policy. We would be merely responding to the harm they have caused.

Excerpted with edits; more at: https://www.ft.com/content/c72fac7b-4b0c-4981-8bc8-8999bde17900

3b. “Trump’s Tariffs,” Ana Swanson, New York Times (The Morning – opinion) Nov. 21, 2024

President-elect Donald Trump calls tariffs “the most beautiful word in the dictionary.” He has talked about them again and again as a fix for America’s economic relationship with the rest of the world. For Trump, this is a way to spur American manufacturing, create new jobs and lower U.S. trade deficits. He used them liberally in his first term, taxing hundreds of billions of dollars’ worth of metals, solar panels and Chinese goods. While running for president this year, he proposed even larger tariffs — of 60 percent or more on China, and up to 20 percent on most goods from other countries.

Can tariffs accomplish these goals? Perhaps in part. They can certainly encourage more factory production, at least in the specific industries they shield: When the United States put tariffs on steel, clothing and kitchen cabinets in Trump’s first term, companies here generally made more of those things

The incoming president is right on a couple of points: First, tariffs do raise money for the government. The amount they generate has more than doubled since Trump first took office (though it is a tiny percentage of government revenue). Second, the United States has much lower tariffs than most other countries do. Both parties agree that some tariffs help protect industries against unfair competition from China.

But tariffs also have downsides, and those can outweigh the economic benefit. Companies charge Americans more to pay for them. And they are regressive, meaning they place a higher burden on poor families than on rich ones.

Tariffs can also backfire by hurting U.S. manufacturers. American factories use a lot of foreign parts and materials, and tariffs make it more expensive to get these. Trump’s steel and aluminum tariffs, for instance, got U.S. firms to make more metals — but because the price rose, other companies that use metals to make things, like industrial machinery and auto parts, ended up manufacturing less. Imposing tariffs on foreign countries also encourages them to do the same thing to the United States. Suddenly, American exporters lose markets abroad. That costs jobs.

Would tariffs help or hurt the economy? It really depends on their size, and other countries’ reactions. One economist argues that if tariffs were low, maybe 10 percent, Americans might just pay a bit more for their imports — not a huge deal. But if tariffs increase significantly beyond that, he said, it could lead to a 1930s-style trade war, in which countries keep retaliating against one another with higher and higher levies. The price of goods could rise quickly.

Excerpted with edits; more at (paywall): https://www.nytimes.com/2024/11/21/briefing/trumps-tariffs.html

4. “Some Fear Factory Boom Could Suffer Under Trump,” Paul Kiernan, Wall Street Journal, Nov. 2, 2024

In the past few years, the U.S. has experienced an epic factory building boom. That could be at risk, some analysts and Democrats say. The reason: former President Donald Trump’s opposition to the laws that helped make it possible. Private fixed investment in manufacturing structures reached an annual pace of $236 billion in the third quarter, more than double the rate at the height of Trump’s presidency after accounting for inflation. The last period in which factory investment grew this fast was at the height of the space race in the 1960s. Some of that boom appears to be linked to the Chips and Science Act, funneling $53 billion in subsidies and tax credits toward semiconductor manufacturing facilities, and the Inflation Reduction Act, authorizing hundreds of billion dollars in tax credits and loans toward low-carbon technologies. President Biden signed both into law in 2022.

“The charts for this metric are kind of crazy when you look at them,” said Oren Cass, founder of American Compass, a think tank that advocates for Republicans to take up populist economic policies. He said this shows industrial policy, whereby the government encourages strategic or favored economic sectors, can boost the supply side of the economy. “The IRA and the Chips Act have been wildly successful, I think beyond even the Biden administration’s initial expectations,” said Ernie Tedeschi, an economist at the Yale Budget Lab who served as chief economist on Biden’s Council of Economic Advisers.

But Trump has criticized the laws as giveaways. “We put up billions of dollars for rich companies to come in and borrow the money and build chip companies here, and they’re not going to give us the good companies anyway,” Trump said on Joe Rogan’s podcast on Oct. 26. “When I see us paying a lot of money to have people build chips, that’s not the way…You could have done it with a series of tariffs.”

In a September speech to the Economic Club of New York, he vowed to “rescind all unspent funds under the misnamed Inflation Reduction Act.” Some around the Trump campaign have called for repeal of the IRA’s green-energy subsidies. Trump has promised to deliver his own “manufacturing renaissance,” via lower taxes, regulations, and most of all, tariffs of 60% on imports from China and 10% to 20% on imports from everywhere else.

But economists surveyed by The Wall Street Journal predicted that if he is elected, Trump’s policies would lead to lower manufacturing employment than otherwise.

Whether Trump could or would cut funding is unclear. It is unlikely a future Trump administration could claw back grants or loans already paid out. Denying IRA tax credits would require a change to the law that could be difficult for Trump to secure even if Republicans control both Senate and the House of Representatives.

Industry leaders note the Chips Act received bipartisan support, while the IRA has led to so many projects in red states that 18 House Republicans signed a letter to Speaker Mike Johnson (R., La.) urging him not to repeal it. Cass said a future Trump administration is more likely to curb IRA spending than Chips grants, given the latter’s bipartisan support. Johnson on Friday told a reporter that Republicans “probably will” try to repeal the Chips Act if they control Congress and the White House, in a video the Harris campaign promptly shared. He later clarified that the Chips Act was “not on the agenda for repeal” but that Republicans might seek to “further streamline and improve the primary purpose” of the legislation by eliminating regulatory and environmental provisions. But Trump could potentially stop or delay money that has yet to be disbursed, Tedeschi said. Some Biden administration officials warn this could disrupt planned projects.

Excerpted with edits; more at (paywall): https://www.wsj.com/economy/trump-manufacturing-policy-inflation-reduction-act-98a2a40e

5. “Why Venture capital is Indispensable for US Industrial Strategy – Activating Investors to Realize Disruptive National Capabilities,” Michael Brown and Pavneet Singh, Institute for Security and Technology report, October 2024

The geopolitical, economic, environmental, and public health challenges facing the United States are more acute now than at any time since World War II. U.S. policymakers recognize that dual-use technologies are essential to solve these challenges. Venture capital is now the principal engine driving the commercial technology ecosystem, providing the necessary capital and personal networks to translate promising technologies into viable businesses. Thus, venture capital is a critical element to any U.S. industrial strategy centered on technology.

However, venture capitalists optimize their investments for outsized returns and are unlikely to invest in technology that requires significant de-risking, has an uncertain or unformed market, or lacks a capable team. To remain competitive and lead in technologies beyond software where venture funding is more scarce, such as novel energy solutions, quantum information systems, microelectronics, and synthetic biology, U.S. policymakers must prioritize the technologies of

highest national interest. Once prioritized, the government should align programs to assist in forming founding teams, coordinate efforts to create markets and signal demand by making the federal total addressable market (TAM) visible, and reduce technology risk.

To summarize, there are five priority recommendations to align national tech priorities with VC incentives:

Prioritize promising federal research for commercial development

Cultivate an entrepreneurial founding team

Create transparency for the federal total addressable market (TAM)

Demonstrate technology maturity, and

Develop a public capital framework

However, of all the programs the government can put in place to stimulate venture investment, none is more powerful than issuing contracts and orders to signal demand. Where hardware development costs are upwards of billions of dollars, government capital can speed development and demonstrate technology maturity faster. However, for less expensive hardware technologies, even a modest grant, like those from the Defense Department’s National Security Innovation Capital (NSIC) program, demonstrates that more mature technology will attract venture capitalists. By providing the right incentives to attract venture capital in developing the highest priority technologies for national security, the United States can activate investor appetite, leverage hundreds of billions of dollars in private capital, and better realize future disruptive capabilities. With appropriate incentives, the venture capital industry will finance and support developing the national capabilities needed for economic prosperity and global security.

Excerpted with edits; more at: https://securityandtechnology.org/virtual-library/reports/why-venture-capital-is-indispensable-for-u-s-industrial-strategy/

Since 2022, MIT has formed a vision for Manufacturing@MIT—a new, campus-wide manufacturing initiative directed by Professors Suzanne Berger and A. John Hart that convenes industry, government, and non-profit stakeholders with the MIT community to accelerate the transformation of manufacturing for innovation, growth, equity, and sustainability. Manufacturing@MIT is organized around four Grand Challenges:

1. Scaling advanced manufacturing technologies

2. Training the manufacturing workforce

3. Establishing resilient supply chains

4. Enabling environmental sustainability and circularity

MIT’s Bill Bonvillian and David Adler edit this Update. We encourage readers to send articles that you think will be of interest to us at mfg-at-mit@mit.edu.