Manufacturing Update - 21 January 2025

Insights from articles and reports of interest on manufacturing technology, management, policy, and economics in the US and abroad

Table of contents for article summaries below:

A two-decade study from “Critical Technologies Tracker” on long-term world research leadership, shows marked shift from US to China in research leadership

US electric vehicle manufacturing investments, jobs continue to grow - … Investments reach $199 Billion, US jobs top 200,000

China’s hidden tech revolution

China grows car production share from 1% to 39% in past 20 years

German dream of becoming a global chip superpower is fading fast

Labor shortages remain an ongoing concern in many parts of US manufacturing

Barry Naughton on the state of the Xi Jinping economy

1. “ASPI’s two-decade Critical Technologies Tracker: The rewards of long-term research investment,” Jennifer Wong Leung, Stephan Robin, Danielle Cave, Australian Strategic Policy Institute, August 2024

This report accompanies a major update of ASPI’s Critical Technology Tracker website (see: https://www.aspi.org.au/report/critical-technology-tracker) which reveals the countries and institutions—universities, national labs, companies and government agencies—leading scientific and research innovation in critical technologies. It does this by focusing on high-impact research—the top 10% of the most highly cited papers—as a leading indicator of a country’s research performance, strategic intent and potential future science and technology (S&T) capability. Now covering 64 critical technologies and crucial fields spanning defense, space, energy, the environment, artificial intelligence (AI), biotechnology, robotics, cyber, computing, advanced materials and key quantum technology areas, the Tech Tracker’s dataset has been expanded and updated from five years of data (previously, 2018–2022) to 21 years of data (2003–2023).

These new results reveal the stunning shift in research leadership over the past two decades toward large economies in the Indo-Pacific, led by China’s exceptional gains. The US led in 60 of 64 technologies in the five years from 2003 to 2007, but in the most recent five years (2019–2023) is leading in seven. China led in just three of 64 technologies in 2003–2007 but is now the lead country in 57 of 64 technologies in 2019–2023, increasing its lead from our rankings last year (2018–2022), where it was leading in 52 technologies.

India is also emerging as a key center of global research innovation and excellence, establishing its position as an S&T power. That said, the US, the UK and a range of countries from Europe, Northeast Asia and the Middle East have maintained hard-won strengths in high-impact research in some key technology areas, despite the accelerated efforts of emerging S&T powers.

This report examines short- and long-term trends to generate unique insights. The results show the points in time at which countries have gained, lost or are at risk of losing their global edge in scientific research and innovation. The historical data provides a new layer of depth and context, revealing the performance trajectory different countries have taken, where the momentum lies, and also where longer-term dominance over the full two decades might reflect foundational expertise and capabilities that carry forward even when that leader has been edged out more recently by other countries.

China’s new gains have occurred in quantum sensors, high-performance computing, gravitational sensors, space launch and advanced integrated circuit design and fabrication (semiconductor chip making). The US leads in quantum computing, vaccines and medical countermeasures, nuclear medicine and radiotherapy, small satellites, atomic clocks, genetic engineering and natural language processing. China’s global lead covers a range of crucial technology fields spanning defense, space, robotics, energy, the environment, biotechnology, artificial intelligence (AI), advanced materials and key quantum technology areas.

India now ranks in the top 5 countries for 45 of 64 technologies (an increase from 37 last year) and has displaced the US as the second-ranked country in two new technologies (biological manufacturing and distributed ledgers) to rank second in seven of 64 technologies. Another notable change involves the UK, which has dropped out of the top 5 country rankings in eight technologies, declining from 44 last year to 36 now. Besides India and the UK, the performance of most secondary S&T research powers (those countries ranked behind China and the US) in the top rankings is largely unchanged, including: Germany (27), South Korea (24), Italy (15), Japan (8) and Australia (7).

We have continued to measure the risk of countries holding a monopoly in research for some critical technologies, based on the share of high-impact research output and the number of leading institutions the dominant country has. The number of technologies classified as ‘high risk’ has jumped from 14 technologies last year to 24 now. China is the lead country in every one of the technologies newly classified as high risk—putting a total of 24 of 64 technologies at high risk of a Chinese monopoly. Worryingly, the technologies newly classified as high risk include many with defense applications, such as radar, advanced aircraft engines, drones, swarming and collaborative robots and satellite positioning and navigation.

In terms of institutions, US technology companies, including Google, IBM, Microsoft and Meta, have leading or strong positions in artificial intelligence (AI), quantum and computing technologies. Key government agencies and national labs also perform well, including the National Aeronautics and Space Administration (NASA), which excels in space and satellite technologies. The results also show that the Chinese Academy of Sciences (CAS)—thought to be the world’s largest S&T institution—is by far the world’s highest performing institution in the Critical Tech Tracker, with a global lead in 31 of 64 technologies (an increase from 29 last year).

The US is losing the strong historical advantage that it has built: Over the 21-year period, the US has been unable to hold its research advantage. In the early to mid-2000s, the US was by far the dominant research power. Its performance between 2003 and 2007 saw it leading in research for 60 out of 64 technologies. Over two decades, however, that research lead has slipped to only seven technologies (in the 2019–2023 ranking). Some notable holdouts include quantum computing and vaccine and medical countermeasures, in which the US still maintains a dominant position. The knowledge, expertise and institutional strengths built over decades of investment and pioneering research are likely to continue to benefit the US in the short term, but China is catching up rapidly through an unsurpassed investment in its own S&T areas and top-performing institutions, especially in key defense and energy technology areas.

Excerpted with edits; more at (paywall): https://www.aspi.org.au/report/aspis-two-decade-critical-technology-tracker

2. “US Electric Vehicle Manufacturing Investments, Jobs Continue to Grow - … Investments Reach $199 Billion, US Jobs Top 200,000,” Environmental Defense Fund and WSP USA (report), August 20, 2024

Thanks largely to supportive federal policies led by the Inflation Reduction Act, America is still seeing strong, steady growth in electric vehicle and battery manufacturing. electric vehicle (EV) manufacturing investments over the last nine years has now reached $199 billion – and 63% of that came after passage of the IRA. Manufacturers have announced 201,900 U.S. EV-related jobs linked to that investment. EV and battery manufacturing could also generate up to 931,000 additional jobs in the broader economy. The report summarizes the significant private investments in manufacturing EVs, EV components, EV batteries, EV battery components, and EV battery recycling over the last nine years.

The data shows:

Concrete investment in U.S. EV and EV battery manufacturing facilities has grown another $11 billion since the report was last updated in March of this year and has now reached $199 billion.

Federal policies have dramatically expanded and accelerated these investments. 63% of announced EV investments occurred in the last 24 months since passage of the Inflation Reduction Act and 83 % occurred in the last 33 months since passage of the Bipartisan Infrastructure Law. Investment has also been spurred by more than $29 billion in federal, state and local incentives.

Manufacturers have now announced 201,900 U.S. EV-related jobs. Federal investments and incentives that are specifically designed to onshore the EV manufacturing supply chain have substantially expanded and accelerated those new job announcements.

In 2027, U.S. EV manufacturing facilities will be capable of producing approximately 5.8 million new electric vehicles annually. That’s the equivalent of 36% of all vehicles sold in the U.S. in 2023.

In 2028, U.S. battery manufacturing facilities will be capable of producing 1,164 gigawatt hours of EV batteries. That’s enough to supply batteries for 13.2 million new electric passenger vehicles each year.

Georgia and Michigan are still the leading states in the U.S. for both EV investments and new jobs, followed by North Carolina (for investments) and Tennessee (for jobs). Ten states now have more than $10 billion in investments and/or more than 10,000 new EV-related jobs: in addition to the four just mentioned they are Illinois, Indiana, Kentucky, Nevada, Ohio and South Carolina.

Excerpted with edits; more at: https://www.edf.org/media/us-electric-vehicle-manufacturing-investments-jobs-continue-grow

3. “China’s Hidden Tech Revolution - How Beijing Threatens US Dominance” Dan Wang, Foreign Affairs, March/April 2023

For the United States and its allies, China’s arrival as a major tech power holds crucial lessons. Unlike the West, China has grounded its technology sector not in glamorous research and advanced science but in the less flashy task of improving manufacturing capabilities. If Washington is serious about competing with Beijing on technology, it will need to focus on far more than trailblazing science. It must also learn to harness its workforce the way China has, in order to bring innovations to scale and build products better and more efficiently. For the United States to regain its lead in emerging technologies, it will have to treat manufacturing as an integral part of technological advancement, not a mere sideshow to the more thrilling acts of invention and R & D.

Many observers are justifiably skeptical about China’s tech leadership. For one thing, the country has created few multinational firms or globally recognized brands. Unlike Japan and South Korea, China has failed to establish new categories of consumer electronics, such as digital cameras or game consoles; nor has it been able to compete with Europe and the United States in automobiles or airliners. Instead, for the most part, Chinese companies have concentrated on making products they can sell at lower price points in the developing world. The relative lack of prominent Chinese brands has reinforced a Western understanding of China as a factory floor rather than a hotbed of innovation.

China also remains well behind the West in several critical technologies. China’s chip industry has a few notable achievements, including in the design of mobile phone chips and certain advanced memory chips. But in the fabrication of logic chips—the processors inside all digital products—Chinese firms are at least five years behind TSMC, the Taiwanese company that is the global leader in advanced semiconductors. They are even weaker when it comes to developing the specialized tools required for making chips. For the all-important lithography machines, used for printing patterns on silicon wafers, and metrology equipment, used for quality control in a production process that demands hundreds of steps, Chinese firms rely overwhelmingly on imports from Japan, the United States, and Europe. And they are barely out of the starting gate in creating the software tools needed to design the most advanced chips. A similar dynamic exists in China’s aviation industry.

Areas of Rapid Progress: But amid these serious vulnerabilities, China is making rapid progress in many other technologies. Chinese firms have quickly gained ground against their European and Japanese counterparts in the production of advanced machine tools such as robotic arms, hydraulic pumps, and other equipment. As the iPhone demonstrates, China now rivals Japan, South Korea, and Taiwan in its mastery of the electronics supply chain. And in the digital economy, despite recent efforts by President Xi Jinping to tighten government control of Internet companies such as Alibaba, Tencent, and Didi, China remains strong. Chinese companies can still offer spirited competition to Silicon Valley’s tech giants, as ByteDance’s TikTok has been doing to Facebook. China leads the world in building modern infrastructure, including ultrahigh-voltage transmission lines, high-speed rail, and 5G networks. In 2019, China became the first country to land a rover on the far side of the moon; a year later, Chinese scientists achieved quantum-encrypted communication by satellite, pushing the country closer to creating unbreachable quantum communications. These achievements are emblematic of China’s steady effort to master more and more difficult tasks.

Solar Dominance: Taken as a whole, then, China’s technological development is considerably more dynamic than the country’s image suggests. One of China’s major tech triumphs in recent years has been in renewable power equipment. When a commercial market emerged for solar technologies early in the twenty-first century, most innovations came from the United States, and it seemed logical that U.S. firms would drive the industry. In 2010, however, China’s State Council, the central government’s executive branch, designated solar power generation as a “strategic emerging industry,” triggering a cascade of government subsidies and business creation, much of it aimed at expanding manufacturing capacity. In the process, Chinese firms learned the basics of solar photovoltaics and began to improve on existing methods of producing them. Today, Chinese firms dominate almost every segment of the solar value chain—from processing polysilicon used in solar cells to assembling solar panels. They have also advanced the technology itself. Chinese solar panels are not only the cheapest on the market; they are the most efficient. The breathtaking decline in solar costs over the past decade has been driven by manufacturing innovations in China.

EV Batteries: Over the last few years, Chinese firms have also staked out strong positions in the production of large-capacity batteries that power electric vehicles. As the world moves away from internal combustion engines, advanced battery technology has become the most critical component in car manufacturing. China has led the way: CATL, a Chinese company founded in 2011, is now the biggest battery manufacturer in the world, partnering with major car companies such as BMW, Tesla, and Volkswagen. In addition to having far greater manufacturing capacity than its rivals—which matters for lowering costs—CATL has taken the lead in developing new and more efficient chemical mixtures, for example in its sodium-ion batteries, which can be produced without using scarce lithium and cobalt minerals.

Manufacturing Strength is Key: China has not achieved dominance in such industries as solar components, EV batteries, and electronics in a vacuum. This rapid progress connects directly to the country’s strengths in manufacturing and quality control. From the early 1990s to today, the Chinese workforce has moved from producing simple toys and textiles to conducting the extraordinarily complex operations needed to produce sophisticated electronics such as the iPhone. Along the way, Chinese firms have often made significant advances of their own: in China, tech innovations have come not from universities and research labs but through the learning process generated by mass production itself. At the heart of the country’s ascendancy in advanced technology, then, is its spectacular capacity for making things. Although there is some truth to all these claims, they are not sufficient to account for China’s rise.

Manufacturing Ecosystem: Instead, the most important factor in China’s burgeoning tech industries is its manufacturing ecosystem. Over the past two decades, China has developed an unrivaled production capacity for tech-intensive industries, one that is characterized by a deep labor pool, dense clusters of suppliers, and extensive government support. This strength draws in part on China’s industrial history. In earlier decades, the government gave industry special importance: disastrously during Mao Zedong’s Great Leap Forward, and more effectively under Deng Xiaoping in his Four Modernizations. Beginning in the 1990s, central government initiatives were less important than market drivers, with China’s manufacturing capacity taking off in the wake of the country’s accession to the World Trade Organization in 2001.

Over the past decade, Xi has put China’s industrial obsession into overdrive. Two years after taking office, he launched Made in China 2025—a sweeping policy framework aimed at lifting China’s manufacturing base from labor-intensive industries to high-technology sectors. And in 2021, in its latest five-year plan, the central government announced a campaign to turn China into a “manufacturing superpower.” That is not an idle goal: over the past few decades, Beijing has directed vast sums of cheap credit and energy to advanced tech firms, even when they are years away from profitability.

Scale-up Subsidies and Support: The solar industry is a case in point. By showering subsidies on all comers, the government encouraged too many firms to enter the field. But it also provoked greater entrepreneurial risk-taking, creating a brutally competitive industry in which the strong muscled out the weak. As a result, Chinese firms today dominate a strategic industry that the rest of the world depends on. This approach—promoting manufacturing to the point of excess capacity—is in sharp contrast to the economic orthodoxy in much of the West, which stresses high-value activities such as R & D and product branding while downplaying the value of physical production as something that can be done cheaply offshore, often in Asia.

Beijing’s manufacturing-driven approach has become critical to its ability to challenge the West in advanced technology. To understand why, it is crucial to recognize the forces that go into successful innovations. Producing new technology can be likened to preparing an omelet: ingredients, instructions, and a well-equipped kitchen are helpful, but they will not in themselves guarantee a good result. Even people with the fanciest equipment and the most exquisite recipe may not be able to make a delicious omelet if they have never cooked before. An additional element is required: practical experience—skills that can only be learned by doing. These skills can be referred to as process knowledge, and they are part of what has helped China become a major tech innovator.

Manufacturing Process Innovation: Although process knowledge is difficult to measure, it can be gauged by a workforce’s general level of experience and by the creation of clusters of varied industrial activity. China has notable strengths in both. The country’s most significant technological achievement over the past two decades has been its development of a vast and highly experienced skilled workforce, which can be adapted as needed for the most tech-intensive industries. For example, Apple still counts on China as the only country that can call up hundreds of thousands of highly trained workers on short notice, quickly access dense networks of component suppliers, and rely on government support to help solve the manifold problems that come with producing millions of iPhones each year.

Equally striking, however, is the way that China has used foreign firms to help build industrial clusters, or what economist Brad DeLong calls “communities of engineering practice.” American firms such as Caterpillar, General Electric, and Tesla have become large employers in China. And most of Apple’s products are produced by contract manufacturers such as Foxconn and Pegatron, which manage workers in China. Unlike Japan, which maintained a mostly closed market during its decades of postwar growth, China has significantly boosted its industrial rise by learning directly from foreign firms. Despite U.S. President Donald Trump’s trade war, Beijing refrained from significant retaliation against U.S. firms in China, partly because it recognizes the managerial expertise they bring and their transmission of manufacturing skills to Chinese workers.

Skilled Workforce: Through continual exposure to the world’s leading manufacturing processes, Chinese workers have acquired skills they can take to domestic firms. Consider the production of EV batteries. Manufacturing these units requires around a dozen discrete steps, each of which demands a near-perfect handoff from the preceding stage. Chinese engineering managers have gained the process knowledge needed for this task through experience in consumer electronics. This transfer of manufacturing know-how has also been one of the keys to China’s dominance of the solar industry. Goosed by subsidies and aided by their ready access to skilled labor, Chinese firms were soon producing better and cheaper solar panels than their U.S. and German counterparts. And these manufacturing innovations have increasingly defined the global industry: the advances in solar over the last decade have been driven less by breakthroughs in science—America’s specialty—than by driving costs down through more efficient production, which is China’s strength.

Excerpted with edits; more at (paywall): https://www.foreignaffairs.com/china/chinas-hidden-tech-revolution-how-beijing-threatens-us-dominance-dan-wang

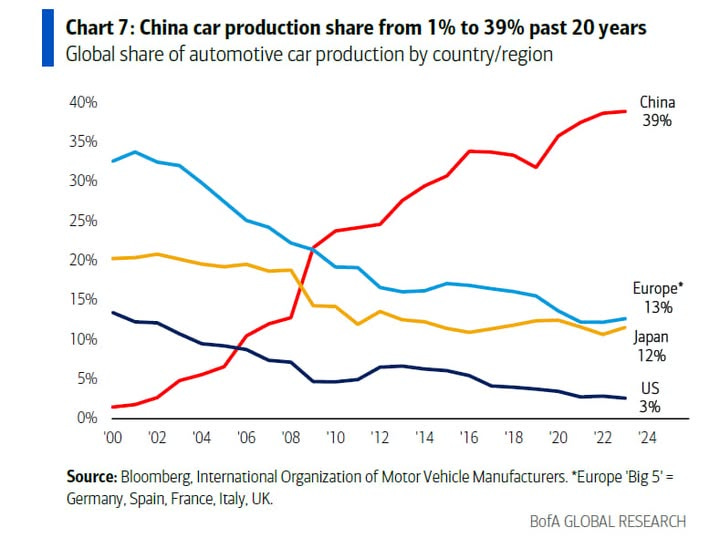

4. “China grows car production share from 1% to 39% in past 20 years,” Bloomberg, Dec. 2024

The US invented mass production and used it to rise to world economic leadership in the 20th century. Today, China’s share of global automotive car production is 13 times that of the US. China makes more cars than the US, Japan, and Europe combined:

Excerpted: https://www.facebook.com/groups/341871730272007/posts/1314198339706003/

5. “German Dream of Becoming a global Chip Superpower is Fading Fast,” Kamil Kowalcze and Christina Kyriasoglou, Bloomberg, Dec. 23, 2024

A vast empty field in Germany’s depressed east is where, for a moment, Olaf Scholz’s ambition to create a lasting economic legacy looked unstoppable.

It was on that plot outside Dresden that the chancellor, wielding a shovel, broke ground for a large plant of Taiwan Semiconductor Manufacturing Company on a hot day in August. He rushed to start digging first, alongside European Commission President Ursula von der Leyen and other dignitaries. Less than a month later, that enthusiasm suffered a crushing blow as another bigger project by rival Intel Corp. to produce some of Europe’s most advanced microchips went awry. That decision to halt a more than €30 billion ($32 billion) investment in Magdeburg, also in the east, followed what officials cite as repeated reassurances of the company’s intention to plow on. The aspiration to turn Germany into a semiconductor superpower, described by insiders as personally driven by Scholz, now looks increasingly hopeless. Aides insist he will stick with it, even though the Intel announcement just robbed his key industrial policy of its centerpiece.

Germany’s attempt at reinvention as a semiconductor hub is part of a worldwide race to win control over the oil of the digital age, and the driving force behind future technologies such as artificial intelligence. The European Union’s goal is to raise market share in global semiconductor output to 20% by 2030 — an aim that seems unattainable. The level in 2024 was just 8.1%, and without further investments, it would fall to 5.9% by 2045, according to analysis by German industry lgroup Zvei and consultancy Strategy&.

Intel’s push to make some of its most modern chips in Germany was touted earlier in 2024 as a “huge leap forward to all of Europe” by then-chief executive officer Pat Gelsinger. While the project is now on a two-year “pause,” many industry insiders consider it as essentially forsaken. The setback was the worst in a series for Scholz. Struggling US chipmaker Wolfspeed Inc. and German automotive supplier ZF Friedrichshafen AG have also rowed back expansion plans, and GlobalFoundries Inc. has relocated some production from Dresden to Portugal.

The site Scholz helped inaugurate in August is part of Germany’s remaining viable joint venture, ESMC, made up of TSMC, Infineon Technologies AG, NXP Semiconductors NV, and Bosch. That’s all that’s tangibly left of his grand vision of attracting international investment to establish a high-tech cluster in the east, create thousands of jobs and cushion the demise of once prosperous sectors like coal mining.

Other European countries have had setbacks too. Intel postponed plans for a Polish factory, and a €7.5-billion joint venture of autochip maker ST Microelectronics and GlobalFoundries in the French town of Crolles is also on hold.

Excerpted with edits; more at (paywall): https://www.bloomberg.com/news/articles/2025-01-07/intel-pullback-undermines-germany-s-dream-of-being-a-semiconductor-superpower

6. “Labor Shortages remain an ongoing concern in many parts of US Manufacturing” Jason Miller, Supply Chain Management, Jan. 13, 2025

Though U.S. manufacturers are not facing the endemic challenges with recruiting labor that they suffered in 2021 and 2022, issues regarding labor shortages are ongoing. The Census Bureau’s Quarterly Survey of Plant Capacity Utilization (QSPC), data through Q3 2024 shows that approximately 20.6% of manufacturing plants in the U.S. that failed to produce at their full capacity cited insufficient supply of labor or labor skills as a key constraint in their production.

I’ve further calculated how Q3 2024 compares to Q3 2018 and Q3 2021. Not surprisingly, almost all sectors report fewer labor challenges today than in Q3 2021—the lone holdout is petroleum & coal products (North American Industrial Classification System - NAICS 324), one of the few sectors where manufacturing output is higher than in 2021. Some sectors such as transportation equipment are citing labor shortages far less frequently today than in 2018, whereas other sectors like chemicals are citing labor shortages far more frequently. One potential explanation is that sectors such as chemical production are operating at a higher rate of capacity utilization than in 2018

Food manufacturing, which is the largest sector of U.S. manufacturing by employment (at over 1.7 million individuals) as well as contribution to for-hire trucking demand—generating roughly 14.5% of all ton-miles of freight hauled by for-hire carriers based on the Commodity Flow Survey—is widely regarded as the sector of manufacturing whose labor is most vulnerable to potential mass deportations.

One indicator to watch closely as we progress through 2025 is the seasonally adjusted quit rate reported by manufacturing firms as part of the Bureau of Labor Statistics Job Openings and Labor Turnover Survey (JOLTS). These data, released through November, show quit rates stabilizing at levels observed in 2017-2019, and down substantially from the peaks observed in 2021 and early 2022. As these data (aggregated quarterly) correlate r = 0.93 with the QSPC data on labor shortages across all manufacturing, they suggest that we are unlikely to see further progress in overcoming labor shortages in 2025.

Excerpted with edits; more at: https://newsletter.smartbrief.com/uyd/editProfile.action?t1=82450471&t2=https%3A%2F%2Fwww.scmr.com%2Farticle%2Flabor-shortages-remain-an-ongoing-concern-in-many-parts-of-u.s-manufacturing

7. “Barry Naughton on the State of the Xi Jinping Economy,” Andrew Peaple, The Wire China, January 5, 2025

(Barry Naughton chairs the Chinese International Affairs at UC San Diego and is one of the world’s leading experts on China’s economy and its transformation over the last half century)

We definitely need to ask what Xi Jinping is trying to achieve with his economic policy. Xi Jinping probably feels that the economy’s performance, in terms of his needs and demands, is actually pretty good. Of course, we don’t know for sure what goes on in Xi Jinping’s mind. But I think we can characterize his approach as this: ‘Billions for tech, but not one cent for bailouts.’

Now, that’s oversimplified. But it captures two elements of what Xi Jinping wants. The first is, high tech and secure development, or what Xi would call high-quality growth. And the other is that he’s very averse to bailing out failing businesses or failing local governments, even when they could potentially be put back on their feet with a bit of a financial helping hand.

In some senses, it’s very natural. Xi has, from an early stage of his administration, insisted that China’s not just looking for GDP growth. They’re looking for growth and security; later, he added that they’re looking for high quality growth. They have a set of developmental desirables that are quite different from just maximizing GDP.

There are a lot of things that Xi Jinping is asking for. But of course, among those, by far the most important is high technology development — and the corresponding development of economic, strategic and scientific self-sufficiency that allows China to be a global power, unconstrained by what he sees as hostile powers, including the United States. That means that Xi Jinping doesn’t really care about what Chinese people want to buy and want to make, because that would be just ordinary GDP. He’s asserting that there’s something more fundamental than that: high quality GDP, which is determined, at the end of the day, by Xi Jinping himself. That’s a very strong, deeply rooted tendency of his.

And it’s really very similar to the impulse that drives a planned economy. Of course, China now has a much more efficient set of institutions, and so the government is steering the economy through mostly market compatible instruments. That doesn’t mean they work well, but at least it means they are compatible.

Xi can argue that his policies have prepared China reasonably well to respond to whatever is coming down the road with the new Trump administration. The ironic thing is, they’ve carried out their de-risking and decoupling program, even while they rail against other countries de-risking and decoupling. They’ve actually done a somewhat effective job of insulating their economy and identifying the areas where other economies are dependent on them.

China will not become self-reliant in chips in a reasonable, foreseeable time frame, five to 10 years. But China is making major investments in each link of the entire semiconductor industrial chain, and they’re making progress. That’s not saying as much as it could, because in many of these links, they started with nothing. Making progress means that they’re creating embryonic structures that might develop into cutting-edge facilities in a decade. Of course, in a decade, the semiconductor industry will have moved on. I don’t think anybody could say that that has been a successful industrial policy so far, and it’s been very costly.

[Although Xi decided against a decisive strategy to place the most overstretched real estate firms into bankruptcy, he is bleeding the sector to death, with minimal housing stimulus. The burst real estate bubble is the leading source of declining Chinese growth.] But there is stimulus. We can see it when we try to track investment, which is not easy to do in China. What we see is a big decline in housing investment, with most of that slack taken up by an increase in industrial investment. Between 2019 and 2024, total fixed asset investment cumulatively has only grown by about 20 percent, so that’s 3-4 percent per year: but investment in some of the big high tech sectors has more than doubled during that time. There’s been a big shift in the composition of investment, towards high tech industry. And if you maintain a certain limit on the amount of deficit the government is willing to bear, and if you say that credit has to be allocated first and foremost to high-tech industries, there’s not that much left over for other kinds of stimulus that would be more effective.

So, there is a stimulus policy, hiding in plain sight. It’s one that is constrained to be a high-tech industrialization investment program. That may or may not work in terms of developing these industries, but it doesn’t provide a very effective stimulus — because it doesn’t create much employment, it doesn’t create much profit, it doesn’t create many new income streams, and so it doesn’t have stimulus multiplier effects. It creates a certain amount of demand for the immediate product that gets the investment put into it. After that, it’s a sort of a wet thud in terms of its impact on the rest of the economy.

[Another economic factor is that] China abandoned the peaceful rise policy that it had in the first part of the century, and adopted a set of policies to play a greater role on a global stage — while essentially eroding the basis of the American system, and pre-positioning themselves to be in some kind of alternative leadership position. To be sure, the U.S. also contributed to this, especially by going to war in Iraq [in 2003]. These changes were also deeply destabilizing [for the world economy].

Excerpted with edits; more at: https://www.thewirechina.com/2025/01/05/barry-naughton-on-the-state-of-the-xi-jinping-economy/

Since 2022, MIT has formed a vision for Manufacturing@MIT—a new, campus-wide manufacturing initiative directed by Professors Suzanne Berger and A. John Hart that convenes industry, government, and non-profit stakeholders with the MIT community to accelerate the transformation of manufacturing for innovation, growth, equity, and sustainability. Manufacturing@MIT is organized around four Grand Challenges:

1. Scaling advanced manufacturing technologies

2. Training the manufacturing workforce

3. Establishing resilient supply chains

4. Enabling environmental sustainability and circularity

MIT’s Bill Bonvillian and David Adler edit this Update. We encourage readers to send articles that you think will be of interest to us at mfg-at-mit@mit.edu.